Hello Book

- Home

- Our Services

- Hello Book

About Us

Contact Us

Visit Us Daily

5A Crescent Road, Epsom

Have Any Questions?

+64 21681919

Mail Us

kelly@epsomfinanceltd.com

Hello Book

Talking to someone who gets it really makes a difference.

Kelly Liu, Financial Adviser

021 681 919 | kelly@epsomfinanceltd.com

23 Gardner Road, Epsom, Auckland, 1023, New Zealand

FSPR Number: 653571

Our promise.

Five things…

You are in

good hands.

Access to over 20+ banks and lenders

all in one place.

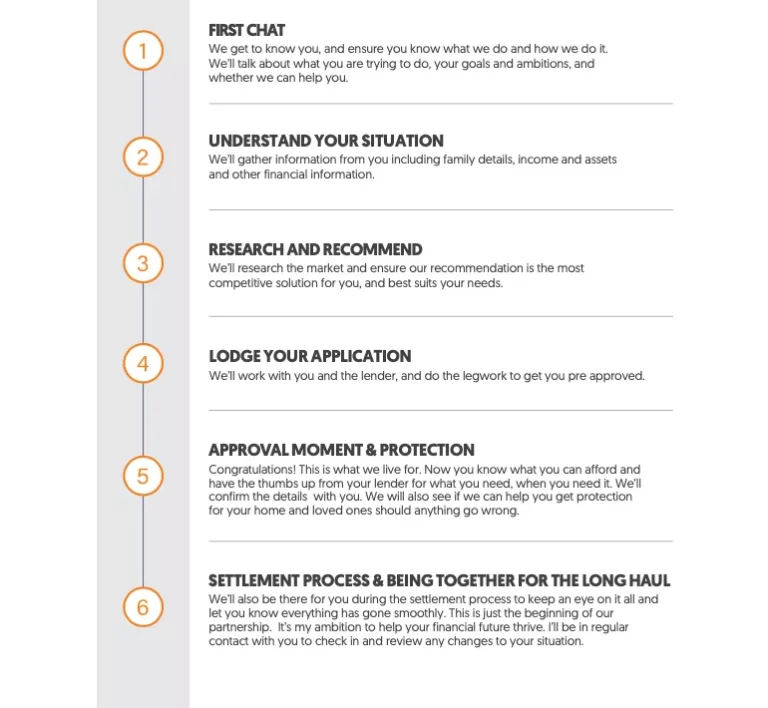

How we will

work together

Everything taken

care of.

Disclosure guide.

Here is some key information you need to know to help you understand what type of advice I am able to give you, so that you can make an informed and confident choice when engaging me.

Details about me and my Financial Advice Provider

I am a Financial Adviser. I give advice on behalf of a Financial Advice Provider. My details are set out below.

Full Name: Kaining Liu

Address: 23 Gardner Road, Epsom, Auckland, 1023, New Zealand Phone: 021 681 919

Email: kelly@epsomfinanceltd.com

FSPR Number: 653571

Name of Financial Advice Provider: Epsom Finance Limited

Trading as: Epsom Finance

FSPR Number: 1004274

Address: 23 Gardner Road, Epsom, Auckland, 1023, New Zealand Phone: 021681919

Email: kelly@epsomfinanceltd.com

My Financial Advice Provider is a member of NZ Financial Services Group Limited

Licensing Information

My Financial Advice Provider is authorised to provide a financial advice service under a current financial advice provider licence issued by the Financial Markets Authority in the name of: NZ Financial Services

Group Limited.

FSPR Number: 286965

Nature and scope of my advice

The information below will help you understand what type of advice I can provide to you.

- I can help you choose and apply for a loan that is suitable for your purpose from a panel of lenders shown below.

- Once we have chosen a lender and loan terms that are suitable for you. I will help you to obtain an approval.

- I may also be able to help you maintain your loan, for example assisting you with re-fixing your loan.

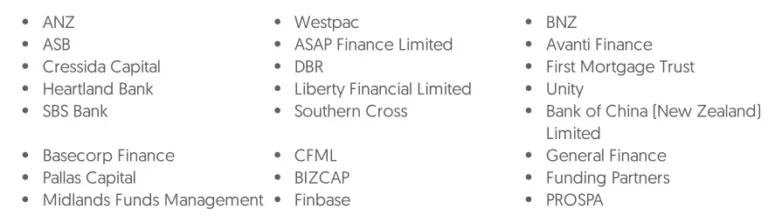

Banks and lenders I use

I source loans from a panel of lenders. The current lenders I can use are:

Products I can advise on

The types of financial products | can give advice on are:

What else I can help you with

I can help you with other services through my referral partners to make it easier for you. However I am not able to give advice on the products they offer and I have not checked to see if they can meet your specific needs. You are free to use other providers of vour choice or undertake your own research.

I am unable to offer legal or tax advice and recommend that you consult your solicitor or accountant for this type of advice.

Fees and expenses

Generally, you won’t be charged any fees for the financial advice I provide to you. This is possible because, on settlement of a loan, the lender usually pays commission to me, which is explained in the commission section of this Disclosure Guide. Any exceptions to this general position are explained below. If these exceptions apply to you, I will let you know.

One-off fees

I may charge you a one-off fee if the following occurs:

[a] There’s no commission: If you request that I provide financial advice and I do not receive a commission from the lender, I may charge you a one-off fee. Any such fee would be agreed and authorised by you in writing before I complete the services, and would be based on an estimate of the time spent providing the advice.

This may arise in the rare event that you request that I provide services in relation to either a product that is offered by a lender for which I do not hold an accreditation, or a product that is outside my usual arrangements with my approved lenders.

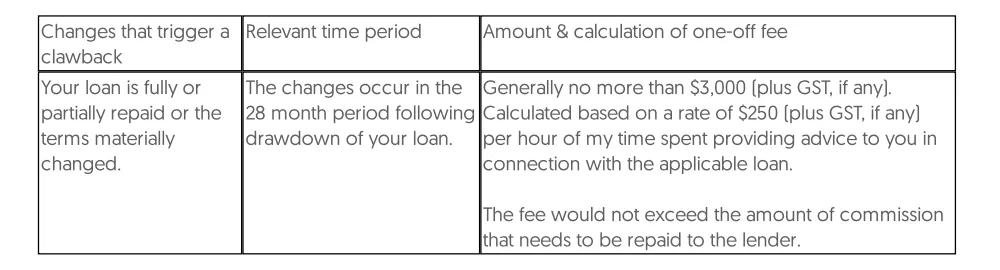

[b] Commission has to be repaid: If you make certain changes to your loan, the lender can require me to repay them the commission I received for your loan – this is called a ‘clawback’ and can be up to 100% of the commission. If this occurs. I may charge you a one-off fee. Set out below are the circumstances in which this would apply and the fee that would be charged to you.

You will be invoiced for any one-off fee and will be given 30 days to make payment.

Adviser fee

Some lenders charge a fee which is capitalised for added] to the amount of your loan. This fee is normally calculated as a percentage of your loan at drawdown, but can be a flat fee. Please see tables 1 & 2 at the back of the guide for further information.

Commissions & incentives

Commissions & incentives that apply to me:

On the settlement of a loan, the lender usually provides me with a commission payment.

The commission is generally an upfront commission payment, but an ongoing commission payment may also be paid by the lender. The upfront commission is calculated as a percentage of the loan at drawdown.

An ongoing commission is calculated as a percentage of the loan outstanding at the relevant time.

I may also receive a fixed-rate rollover fee from the lender if I assist in refixing your loan.

The maximum percentage that each lender uses to calculate upfront and ongoing commissions, and the maximum fixed rate rollover fees (refix fees), are set out in Table 3 at the back of this guide. If there are any variations to these percentages or other commission payments that may apply, specific to your loan application, I will disclose this to you as part of my advice process.

I may also receive a referral fee or commission payment if I refer you to our referral partners.

Commission payments or referral fees can be paid in different ways:

- Paid in full to a financial adviser.

- Shared between two or more financial advisers.

- Paid to an employer who then pays a financial adviser a salary.

- Paid in full to a financial adviser’s company, from which the financial adviser takes drawings or profit share.

- Shared with a licence holder to cover the costs of the services they provide.

I can provide you with more information to explain which option applies to me.

Occasionally | may receive incentives or rewards from lenders or referral partners. For example, lenders may provide us with gifts, tickets to events or other incentives.

I manage the conflicts of interest arising from these commission payments, referral fees or incentives by:

- Following an advice process that ensures I understand your needs and goals so that I always recommend the best loan for you regardless of the type and amount of commission or other payments

I may receive. - Ensuring the amount of any loan is in accordance with your identified needs.

- Providing you with tables showing commission rates and types by lender.

- Undertaking regular training on how to manage conflicts of interest.

Privacy policy & security

I will collect personal information about you in accordance with my Privacy Policy. I regard client confidentiality as of paramount importance. I will not disclose any confidential information obtained from or about you to any other person, except in accordance with my Privacy Policy.

Our Privacy Policy outlines that we may share your personal information with NZ Financial Services Group Limited for audit purposes. This ensures that we deliver services in our best interests and comply with current regulations. If you disagree with this, please email team@nzfsg.co.nz and inform me, as I won’t be able to provide financial advice services to you.

The electronic platform I use to store your personal information is secure and runs on Amazon Web Services.

Complaints Process

If you have a complaint about my financial advice or the service I gave you, you need to tell me about it.

You can contact my internal complaints service by phoning, or emailing me (Subject line: Complaint – Your Name]. Please set out the nature of your complaint, and the resolution you are seeking. I aim to acknowledge receipt of this within 24 hours. I will then record vour complaint in our Complaints Register and will work with you to resolve vour complaint. I may want to meet with vou to better understand vour issues. I aim to provide an answer to you within 7 working days of receiving your complaint. If we cannot agree on a resolution vou can refer vour complaint to our external dispute resolution service. This service is independent and will cost you nothing and will assist us to resolve things with you. The name of this service and their contact details are:

Financial Services Complaints Limited (FSCL) – A Financial Ombudsman Service

complaints@fscl.org.nz

0800 347 257

https://www.fscl.ora.nz/

PO Box 5967 Wellinaton 6140

My duties

I am bound by and support the duties set out in the Financial Markets Conduct Act 2013. These duties are to:

- Meet the standards of competence, knowledge, and skill set out in the Code of Professional Conduct for

Financial Advice Services (Codel. - Give priority to my client’s interests.

- Exercise care, diligence, and skill.

- Meet the standards of ethical behaviour, conduct, and client care set out in the Code.

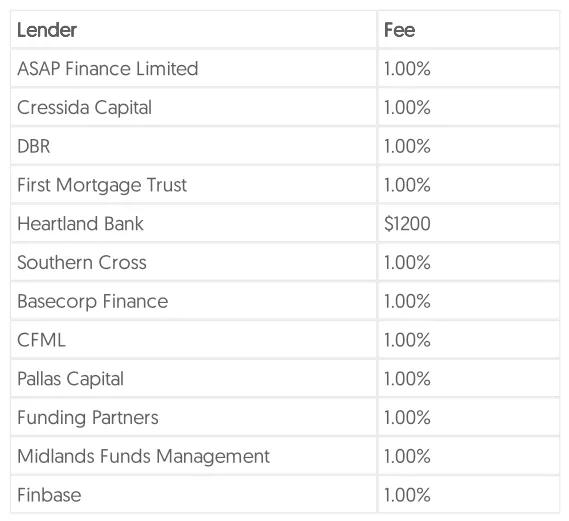

Table 1 - Adviser fee (no commission)

The maximum percentage rates, or maximum fee charged for each lender is set out below. This fee is then paid to me by the lender, instead of a commission payment.

Table 2 - Adviser fee (plus commission)

The maximum percentage rates, or maximum fee charged for each lender, are set out below. This fee may be paid to me by the lender, in addition to a commission payment.

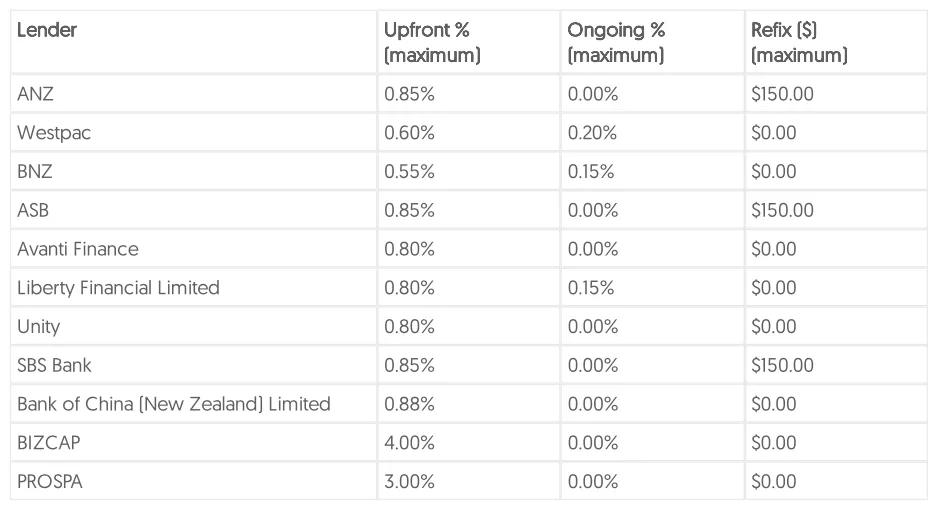

Table 3 - Adviser commission

The maximum percentage and dollar rates for each lender is set out below. This commission payment is then paid to me by the lender.

Availability of Information

This information can be provided in hardcopy upon your request.